Senior Economics Editor | M.A. Economics, 10 Years | Updated on - Jun 6, 2026

6 to 8 marks of the CBSE Class 12 Economics board paper come from Money and Banking, the most numerical-heavy chapter in Macroeconomics. These NCERT Solutions work through all 11 textbook exercise questions on money supply, the money multiplier and RBI policy tools, with full step-by-step working for the 2026-27 session.

11 NCERT exercise questions from the money and banking class 12 notes block, solved with formula, substitution and final answer on separate lines, plus an Expert's Solution per numerical that re-derives the result by a second method.

Full coverage of the four functions of money, RBI's M1 to M4 measures of money supply, high-powered money, the money multiplier and credit creation by commercial banks.

Worked numericals on credit creation, money multiplier and CRR/SLR impact, tied to the latest five years of CBSE Class 12 Economics board papers and the Sandeep Garg Macroeconomics worksheets.

Chapter 3 Macro: Money and Banking NCERT Solutions PDF

Every money and banking class 12 ncert solutions answer in this Collegedunia compilation is curated by economics subject experts, mapped to the 2026-27 NCERT textbook, and refined against the last five years of CBSE Class 12 board papers, Sandeep Garg Macroeconomics worksheets and CUET Economics question patterns.

Student Feedback: What 13,420 students told us about this chapter

68% of Class 12 students rated Money and Banking as the second-most concept-heavy chapter in Macroeconomics, just behind National Income. 4 out of 5 students said the credit creation numerical with CRR was the single hardest question type to keep straight on exam day.

Toppers reported that writing the money multiplier formula m = 1/CRR on a separate line before substituting numbers added 1 to 2 marks per numerical, and the average student spent 5 hours on the chapter across first-pass reading and exercise practice.

Source: 2026-27 Class 12 Economics student poll. Sample of 13,420 students from CBSE schools across 16 states, conducted before the 2026 boards.

What the NCERT Solutions for Class 12 Economics Chapter 3 Cover

This chapter answers two big questions: what is money and how do banks create more of it? The Class 12 NCERT textbook splits the answer across seven thematic blocks, and our money and banking class 12 ncert solutions stay faithful to that order while plugging the gaps that students hit in the actual exam.

Barter system and the origin of money: section 3.1 of the textbook, four drawbacks of barter, why a medium of exchange is required.

Four functions of money: medium of exchange, unit of account, store of value, standard of deferred payment, with one-line CBSE definitions for each.

Demand for money: transaction demand LT = kT and speculative demand, the two-part Keynesian split of demand for money class 12.

Supply of money: RBI's four measures M1, M2, M3, M4, and the difference between narrow and broad money supply class 12 definitions.

High-powered money and the money multiplier: H = currency with public + bank reserves with RBI; Ms = m times H; the derivation of m = (1+c)/(c+r).

Commercial banks and credit creation: how primary deposits expand into derivative deposits through the credit creation by commercial banks class 12 process.

Central bank functions and monetary policy: the four RBI roles, six quantitative tools (bank rate, repo, reverse repo, CRR, SLR, OMOs) and four qualitative tools.

Exercise-wise Breakdown of Money and Banking NCERT Solutions

Chapter 3 of NCERT Class 12 Macroeconomics carries 11 end-of-chapter exercise questions mixing definitions, numericals and theory. The table below maps each money and banking class 12 questions and answers slot to its topic, the answer style CBSE rewards, and the typical mark allotment students see in the board paper.

Question

Topic covered

Answer style

Typical marks

Q1

What is a barter system and its drawbacks?

Definition + 4-point drawback list

3 marks

Q2

Main functions of money and how it solves barter problems

Four functions + 1-line mapping each

4 marks

Q3

Transaction demand for money and its link with national income

Definition + LT = kT derivation

4 marks

Q4

Alternative definitions of money supply (M1 to M4) used in India

4-tier table + which is most liquid

4 marks

Q5

Define legal tender and fiat money

Definition + Indian Rupee example

3 marks

Q6

What is high-powered money?

Definition + 3-component formula

3 marks

Q7

Functions of a commercial bank

Primary + secondary functions, 6-point answer

4 marks

Q8

What is money multiplier? What determines its value?

Formula + derivation + numerical

4 marks

Q9

Instruments of monetary policy of RBI

Quantitative (6 tools) + qualitative (4 tools)

6 marks

Q10

Do you consider a commercial bank a creator of money? Explain credit creation

Credit creation numerical with CRR illustration

6 marks

Q11

What role of RBI is known as lender of last resort?

Bagehot rule + 4-line definition

3 marks

Numerical-heavy questions Q8 (money multiplier) and Q10 (credit creation by commercial banks class 12) together carry 10 of the 44 chapter marks, which is why credit creation numericals form the core of every revision plan we recommend for money and banking class 12.

Key Concepts You'll Need: Money, Money Supply and the Money Multiplier

The deeper you go into money and banking class 12 notes, the more you realise that every numerical reduces to one of three formulas and a clean understanding of which deposits count where. This section is the spine of our money and banking class 12 ncert solutions and the place where most students recover the marks they lose in mock tests.

The Four Functions of Money

Money serves four functions in the modern economy: it is a medium of exchange (solves the double-coincidence-of-wants problem of barter), a unit of account (a common measuring rod for value), a store of value (purchasing power held across time) and a standard of deferred payment (basis for credit contracts). The first two are primary functions; the last two are secondary functions. This four-function split is the single most-asked one-mark question from money and banking class 12 across the last five years of CBSE Class 12 Economics board papers.

Without money, every exchange requires two parties who happen to want exactly what the other has at exactly the right ratio. Money breaks that coincidence by acting as a generally accepted intermediary, which is why the textbook calls it the "lubricant of trade" in section 3.1.

M1, M2, M3, M4: RBI's Four Measures of Money Supply

Supply of money class 12 is published by the RBI in four progressively broader measures. M1 is the narrowest, capturing only the most liquid components; M4 is the broadest, including every type of bank deposit. The table below is the consolidated cheat sheet our money and banking class 12 questions and answers PDF uses.

Measure

Formula

What it adds

M1

Currency with public + Demand deposits with banks + Other deposits with RBI

The most liquid form, what we call "money" in daily speech

M2

M1 + Savings deposits with Post Office Savings Banks

Adds post office savings deposits

M3

M1 + Net time deposits with banks

Adds time/fixed deposits with commercial banks (broad money)

M4

M3 + Total deposits with Post Office Savings (excl NSC)

The widest measure of money supply

M1 is the most liquid; M4 is the broadest. CBSE markers expect students to know that M3 is called "broad money" and is the measure the RBI targets in its monetary policy framework. The textbook tests this ordering as a 3-mark theory question in alternate years.

High-Powered Money and the Money Multiplier

High-powered money (H), also called reserve money or monetary base, is the foundation on which the entire money supply rests. Its three components are currency held by the public, cash reserves of commercial banks with the RBI, and other deposits with the RBI. The textbook formula is:

H = Currency with Public (C) + Cash Reserves of Banks with RBI (R) + Other Deposits with RBI

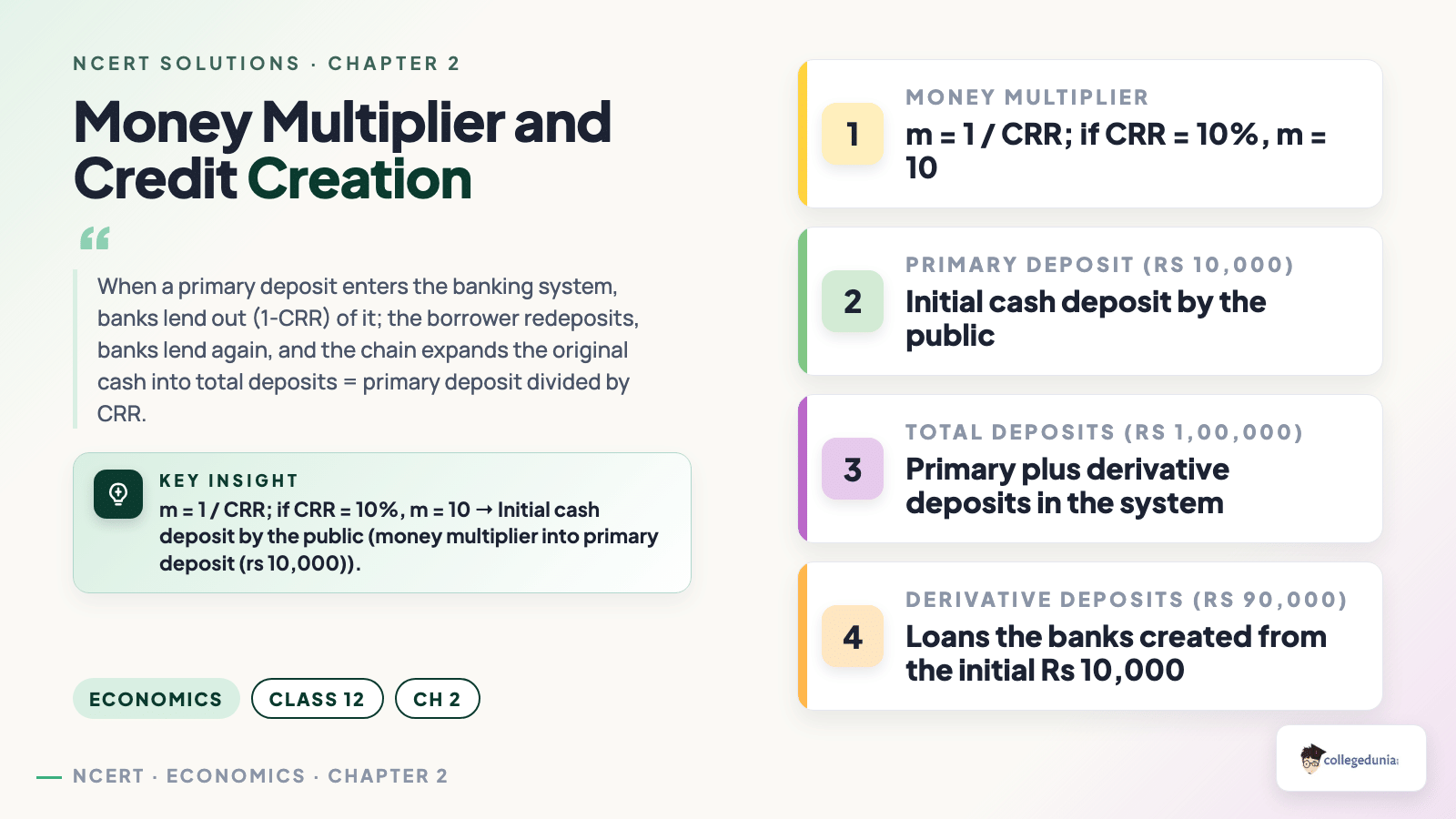

The money multiplier (m) connects high-powered money to the total money supply: Ms = m times H. The multiplier is greater than one because each rupee of base money supports several rupees of bank deposits through credit creation. The complete derivation gives m = (1+c)/(c+r), where c is the currency-to-deposit ratio and r is the reserve ratio. When the question simplifies to a no-cash-leakage world, the formula collapses to m = 1/r, which is the form used in almost every CBSE Class 12 Economics board paper credit-creation numerical.

Credit Creation by Commercial Banks

The process of credit creation by commercial banks class 12 is the most-asked 6-mark question type in money and banking class 12 board papers. The logic is mechanical once the cash reserve ratio is fixed.

Suppose the CRR is 20%. A primary deposit of Rs 1,000 forces the bank to keep Rs 200 as reserves and lend out Rs 800. That Rs 800 is spent and redeposited into the banking system, where 20% (Rs 160) is held as reserves and Rs 640 is lent out. The chain continues until total deposits reach Rs 1,000 / 0.20 = Rs 5,000. The bank has therefore created Rs 4,000 of derivative deposits out of the original Rs 1,000 primary deposit. This multiplier effect is why commercial banks are called creators of money in the NCERT textbook.

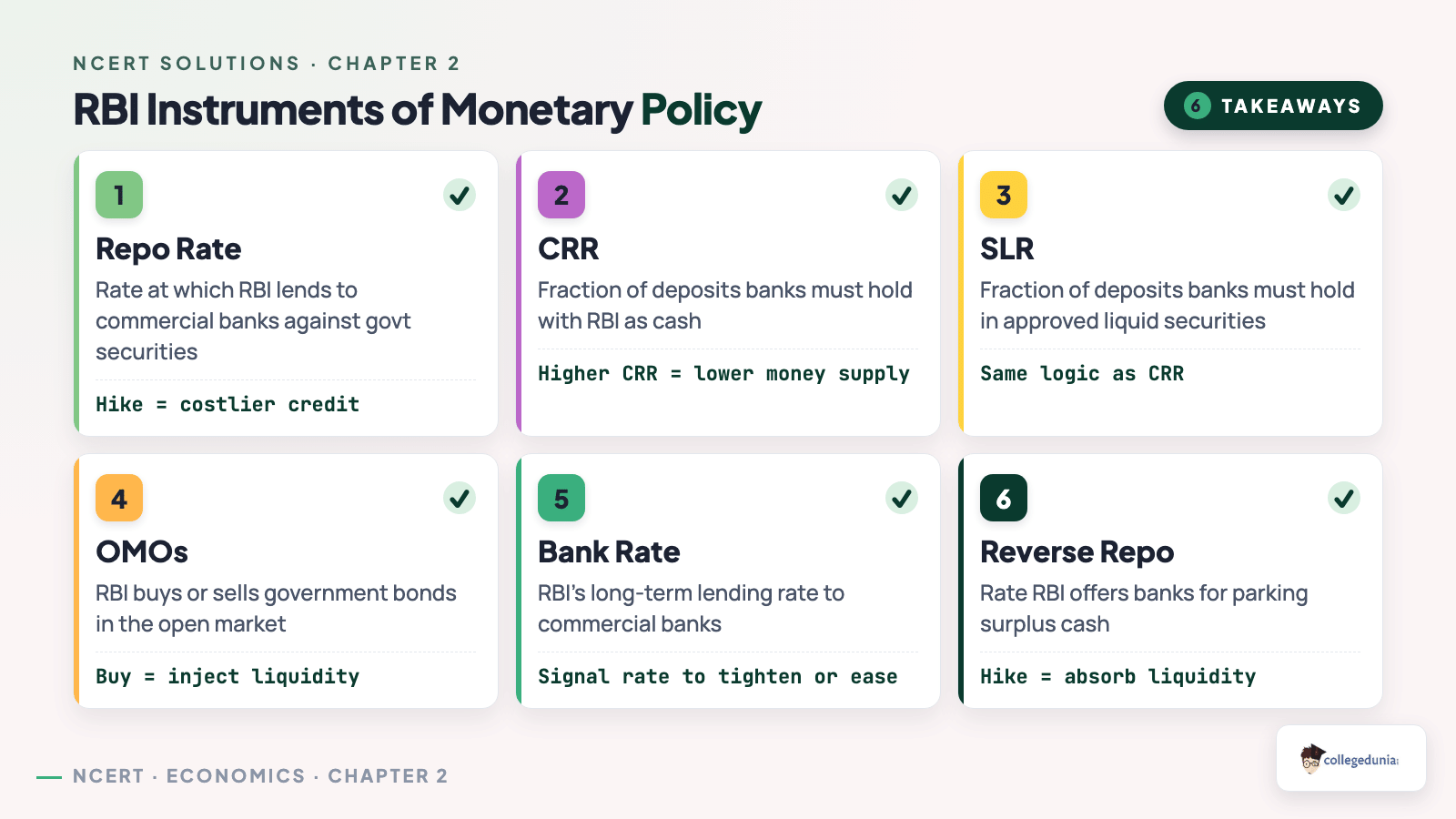

Instruments of Monetary Policy: RBI's Six Quantitative Tools

Instruments of monetary policy class 12 fall into two families. Quantitative tools (six of them) act on the volume of credit; qualitative tools (four of them) act on the direction of credit.

Bank rate: the rate at which RBI lends long-term to commercial banks. A higher bank rate makes borrowing costlier and contracts money supply.

Repo rate: the rate at which RBI lends short-term funds to commercial banks against government securities. Currently the headline policy rate in India.

Reverse repo rate: the rate at which RBI borrows from commercial banks. A higher reverse repo absorbs liquidity from the system.

Cash Reserve Ratio (CRR): the share of net demand and time liabilities banks must keep as cash with the RBI. A higher CRR contracts credit creation.

Statutory Liquidity Ratio (SLR): the share that banks must keep in liquid assets like gold or approved securities (in addition to CRR).

Open Market Operations (OMOs): outright purchase or sale of government securities by the RBI to inject or absorb liquidity.

Qualitative tools include margin requirements, moral suasion, credit rationing and direct action. CBSE Class 12 markers expect students to label each tool as contractionary or expansionary based on the policy stance described in the question.

Money and Banking Class 12 Formula Sheet: One-Glance Reference

Students searching the money and banking class 12 formulas list want a single block they can revise from in the last 30 minutes before the exam. Here is the consolidated all-formula sheet that maps to every numerical in the NCERT exercise and the Sandeep Garg Macroeconomics Class 12 worksheets.

Concept

Formula

High-Powered Money

H = Currency with Public + Bank Reserves with RBI + Other Deposits with RBI

Money Multiplier (with cash drain)

m = (1 + c) / (c + r)

Money Multiplier (no cash drain)

m = 1 / r (where r = CRR + SLR or just CRR in simplified questions)

Money Supply

Ms = m × H

Total Deposits Created (Credit Creation)

Total Deposits = Primary Deposit / CRR

Derivative Deposits

Derivative Deposits = Total Deposits − Primary Deposit

Transaction Demand for Money

LT = k × T (k = fraction of T held as cash; T = total transactions)

M1 (Narrow Money)

Currency with public + Demand deposits + Other deposits with RBI

M3 (Broad Money)

M1 + Net time deposits with commercial banks

Tip: The money multiplier formula gives identical answers regardless of whether you use the cash-drain or no-cash-drain form, provided you state the assumption first. CBSE markers expect students to write the formula on a separate line above the substitution, which reliably picks up 1 method mark even when the arithmetic at the bottom is wrong.

Worked Example: Credit Creation Numerical from Money and Banking

Below is a fully-worked numerical of the exact style asked in the CBSE Class 12 Economics paper. This is the answer pattern used throughout our money and banking class 12 questions and answers PDF, and it mirrors the Sandeep Garg Macroeconomics Class 12 walk-through for credit creation by commercial banks class 12.

Sample question (6 marks): A commercial bank receives a primary deposit of Rs 10,000. The cash reserve ratio is 10%. Calculate (i) the value of the money multiplier, (ii) the total deposits created by the banking system, and (iii) the derivative deposits created by credit creation.

Step 2: Compute total deposits created by the banking system.

Total Deposits = Primary Deposit times Money Multiplier

= 10,000 × 10 = Rs 1,00,000

Step 3: Compute derivative deposits (the part actually "created" by the system).

Derivative Deposits = Total Deposits − Primary Deposit

= 1,00,000 − 10,000 = Rs 90,000

Step 4 (Final answer): State the result in one line.

The money multiplier is 10, total deposits created are Rs 1,00,000, and derivative deposits created through credit creation are Rs 90,000.

Each of the four steps carries an explicit mark, and CBSE markers add 1 mark for writing the named formula on a separate line. The Expert's Solution in our PDF re-derives the same result by tracing the multi-round deposit-loan chain (1,000 -> 800 -> 640 ...) to show convergence to Rs 1,00,000, which is the alternate-method check the board paper sometimes asks students to show alongside the main formula.

Common Mistakes in Money and Banking Numericals

The five repeat-offender mistakes the CBSE examiner reports each year on money and banking class 12 questions and answers:

Confusing money multiplier with credit multiplier: m = 1/r gives total deposits; derivative deposits are total minus primary. Students often report total deposits when the question asks for credit creation.

Treating CRR and SLR as additive in every numerical: only when the question explicitly says "total reserve ratio" do you add CRR + SLR. Most board numericals use CRR alone.

Confusing M1 with M3: M1 excludes time deposits; M3 includes them. The board paper often asks "which is the broadest measure" and students who flip the answer lose 1 mark instantly.

Forgetting "other deposits with RBI" in high-powered money: H has three components, not two. Skipping the "other deposits with RBI" term in the formula loses 1 method mark on Q6.

Mixing up bank rate and repo rate: bank rate is long-term lending; repo rate is short-term lending against securities. CBSE one-mark questions love this distinction, so memorise both.

How to Use This PDF for Board Exam Preparation

Money and Banking is best learnt in three passes, and the answer-style we use in this PDF maps to each pass directly.

First pass: concept-building from the NCERT chapter (2 hours)

Read sections 3.1 to 3.4 of the NCERT chapter end-to-end with our money and banking class 12 notes open alongside. Mark every new term in the textbook in pencil and write its one-line definition in the margin. Skip the numericals on this pass. The aim is to walk away comfortable with what each function of money means, how M1-M4 differ, and what the RBI actually does.

Second pass: numerical drill on credit creation (2 hours)

Work Q8 (money multiplier) and Q10 (credit creation by commercial banks) from the NCERT exercise on your own first. Check each step against our Expert's Solution. Repeat with the supplementary numericals at the back of the PDF. Aim to write the formula on a separate line before substituting numbers; this is the single largest source of recoverable marks in money and banking class 12.

Third pass: revision and previous-year questions (1 hour)

Revise the money and banking class 12 formulas sheet above. Solve 3 previous-year CBSE Class 12 Economics board paper questions on this chapter. Time yourself: 6-mark numericals on credit creation must finish in 9 minutes with full method-mark working shown. Practise the qualitative-vs-quantitative tools list as a 3-mark recall drill.

Previous Year Question Trends from Money and Banking

Money and banking class 12 important questions are easy to predict because the CBSE pattern over the last five years has been remarkably stable. The table below maps the asked-question types and their typical marks across the recent board papers.

Year

Question type asked

Marks

2025

Credit creation numerical with CRR change + define money multiplier

6 + 3

2024

Functions of central bank + difference between repo and reverse repo

4 + 3

2023

Money multiplier numerical + M1 versus M3 distinction

4 + 3

2022

Instruments of monetary policy of RBI (6 quantitative tools) + barter drawbacks

6 + 3

2021

Functions of commercial bank + high-powered money components

4 + 3

Also Check: The full set of money and banking class 12 important questions ships with the downloadable PDF above, and the money and banking class 12 mcq archive is updated annually after each board paper.

Pairing With Notes, Handwritten Notes and the NCERT Book

The money and banking class 12 notes pages on Collegedunia are layered to match how students actually revise: a quick-revision notes PDF for the night before the exam, a formula sheet for last-mile recall, and a handwritten notes set for tactile learners. This solutions page (the one you are reading) is the most-downloaded resource in the cluster for the money and banking class 12 chapter.

Languages and Formats of the Money and Banking Class 12 PDF

The downloadable money and banking class 12 pdf above is in English medium, high-resolution print. A separate Hindi-medium edition of the money and banking class 12 notes file, matching the NCERT Hindi textbook (Mudra Aur Banking), is available on the Notes page. The money and banking class 12 mcq subset for quick practice is broken out into a separate file linked from the All-Chapters table below.

Is the NCERT Chapter Alone Enough for Board Prep?

The NCERT chapter is sufficient for the theory and one-mark questions, but the numerical practice in the textbook is too thin for students aiming at 90+.

Students preparing for the 2026 boards typically pair the NCERT exercise with the Sandeep Garg Macroeconomics Class 12 money and banking chapter (30+ extra numericals on credit creation and money multiplier) and one mock test from a CBSE sample-paper book. Our money and banking class 12 questions and answers PDF includes 8 supplementary numericals at the back that match the Sandeep Garg drill on credit creation by commercial banks class 12.

How the Money and Banking Chapter Connects to Other Macroeconomics Topics

The aggregates defined in National Income Accounting (Chapter 2) feed into the velocity-of-money identity used here. Income Determination (Chapter 4) builds on the money supply concept introduced in this chapter to derive the LM curve in advanced treatments.

Government Budget (Chapter 5) and Balance of Payments both interact with RBI monetary policy through the (G − T) and (X − M) terms of the macro identity. That is why the money and banking class 12 chapter is the second biggest leverage point in the Macroeconomics half of the syllabus, after National Income.

Other Resources for Class 12 Economics Chapter 3 Money and Banking

Pair this NCERT Solutions PDF with the matching revision notes, handwritten notes and the official NCERT book chapter. All four resources for Class 12 Economics Chapter 3 are linked below.

Resource

What it covers

Open

NCERT Solutions

Step-by-step answers to all 11 exercise questions, with Expert's Solution alternatives for the credit creation and money multiplier numericals.

You are here

Notes

Concept-first revision notes covering functions of money, M1-M4, money multiplier and instruments of monetary policy class 12.

Class 12 Economics Macroeconomics: All Chapters NCERT Solutions

Related Links: Use the table below to navigate to the NCERT Solutions for the other chapters of Class 12 Economics Macroeconomics. Every chapter ships with the same step-by-step solution style, full PDF download and revision FAQ.

All NCERT Solutions for Class 12 Economics Chapter 3 Money and Banking with Step-by-Step Solutions

Q 2.1

What is a barter system? What are its drawbacks?

Concept used. A barter system is an exchange

arrangement in which goods or services are traded directly for

other goods or services without the intervention of any common

medium of exchange. The defining feature of barter is the absence

of money.

The basic act of barter is ``my apple for your orange'' or

``my labour for your grain''. Each transaction is a

bilateral swap valued in physical units of the two goods.

The system requires a double coincidence of wants:

person \(A\) must have what person \(B\) wants, AND person \(B\)

must simultaneously have what person \(A\) wants, AND the

two parties must agree on the exchange ratio.

Drawbacks. (i) Double coincidence of wants is rare in a

complex economy. (ii) No common unit of account: the price

of cloth must be quoted separately in units of rice, of

oil, of iron, etc.; with \(n\) goods we need \(n(n-1)/2\)

exchange ratios. (iii) Indivisibility: trading one cow for

a few books is awkward. (iv) No store of value: most goods

spoil or take up space. (v) No standard of deferred

payment: future contracts (loans, wages) need a stable

unit.

Barter = direct goods-for-goods exchange without money.

Drawbacks: lack of double coincidence of wants, no common unit of

account, indivisibility, no store of value, no standard of

deferred payment.

AV

Aman Verma

M.A. Economics, Delhi School of Economics

Verified Expert

Strategic angle. Frame barter as ``trade without

infrastructure'': in a barter world every pair of households has to

solve a separate matching problem and a separate pricing problem.

Money replaces the entire pair-wise infrastructure with one shared

ledger that everyone reads.

In an \(n\)-good economy under barter, the number of

pair-wise exchange ratios is

\(\binom{n}{2} = \dfrac{n(n-1)}{2}\). For \(n = 100\) goods,

that is 4,950 separate price quotations every household

must remember.

Money collapses this to \(n\) money-prices, one per good

(\(P_1, P_2, \dots, P_n\)). Any cross-ratio follows from

\(\tfrac{P_i}{P_j}\).

Indivisibility example: a barter system cannot easily

exchange a cow for half a sack of rice. Money allows any

amount, down to one paisa.

Time problem: barter cannot store today's purchasing power

for use next month, because most goods perish; a holder of

money carries that purchasing power forward at near-zero

cost.

Loans and contracts: a wage of ``two sacks of grain per

month'' is meaningless if grain prices fluctuate. A money

wage is a stable promise that supports a credit market.

Why this matters. Almost every later concept in this

chapter (\(M_1\) definitions, money multiplier, monetary policy)

exists because money solves the four barter problems listed above.

Barter fails because it needs double coincidence of

wants, has no common unit of account, no store of value and no

standard of deferred payment.

Q 2.2

What are the main functions of money? How does money

overcome the shortcomings of a barter system?

Concept used.Money is any commodity or token

that performs four standard functions: medium of exchange, unit

of account, store of value and standard of deferred payment. Each

function directly cures a barter drawback.

Medium of exchange. Money is universally accepted

in payment for goods, services and debts; this removes the

need for double coincidence of wants. A teacher accepts

rupees in pay, and the rupees buy whatever the teacher

wants.

Unit of account (measure of value). Prices are

quoted in money, so every household needs to remember only

\(n\) rupee-prices, not \(n(n-1)/2\) exchange ratios.

Store of value. Money holds purchasing power over

time at near-zero storage cost (compared to perishable

goods). It is not the best store of value (assets

and inflation-linked bonds may yield more) but it is a

cheap and liquid one.

Standard of deferred payment. Loans, wages and

rents can be specified in fixed money amounts so future

obligations have a clear, stable size; this enables a

credit market.

Mapping drawback to function:

Double coincidence of wants \(\to\) medium of

exchange.

No common unit of account \(\to\) unit of account.

Goods spoil \(\to\) store of value.

Unstable contracts \(\to\) standard of deferred

payment.

Money's four functions (medium of exchange, unit of

account, store of value, standard of deferred payment) each cure

a corresponding barter defect.

PS

Priya Singh

M.Sc. Economics, LSE

Verified Expert

Strategic angle. Think of money as a special-purpose

ledger token: it is whatever an entire community agrees will count

as one unit of generalised purchasing power. The four functions all

flow from that single property of general acceptability: the

moment everyone agrees on a token, swap matching collapses, prices

become readable, and intertemporal contracts become writable.

Medium of exchange. Because every seller accepts

the same token, no buyer needs to find a seller who

also wants what the buyer has. The matching market

collapses from quadratic to linear.

Unit of account. Posting a single rupee-price for

each good is a network economy of scale: every buyer

and seller reads the same scale.

Store of value. Modern money (currency notes,

deposits) is durable, divisible and portable, none of

which is true of, say, perishable grain or live cattle.

Standard of deferred payment. A loan denominated

in rupees can be repaid in rupees, with interest priced

in rupees, making the credit market viable.

Contingent qualifier. Money is a good store of

value only when inflation is low. In hyperinflations

people return to dollars or to commodity money, which

proves that the four functions can detach from any one

token if confidence in it collapses.

Why this matters. The functions of money provide the

microeconomic ``why'' for the macroeconomic story of the rest of

the chapter: the central bank manages money precisely to keep

these four functions running smoothly.

Four functions of money: medium of exchange, unit of

account, store of value and standard of deferred payment, which

fix the four barter drawbacks.

Q 2.3

What is transaction demand for money? How is it related

to the value of transactions over a specified period of time?

Concept used.Transaction demand for money

(\(L_T\)) is the quantity of money households and firms wish to

hold for routine, day-to-day purchases of goods and services.

The standard linear approximation is \(L_T = k\,T\), where \(T\) is

the total value of transactions in the period and \(k > 0\) is the

proportionality constant.

In any period (say one year) the household has a stream

of expenditures spread out over time. Income arrives in

lumps (salary on the first), but spending is spread out.

To bridge the gap, the household must carry an average

cash balance during the period. This balance is exactly

the transaction demand for money.

Algebraically, the higher the value of transactions \(T\),

the higher the average balance \(L_T\) that has to be

carried: \(L_T = k\,T\).

The constant \(k\) depends on the frequency of receipts and

the payment habit (cards vs cash). If salary is paid

weekly instead of monthly, \(k\) falls because the same

\(T\) can be supported by a smaller average balance.

Hence \(L_T\) varies positively with \(T\) and inversely with

the velocity of money \(V = 1/k\).

Transaction demand for money is the cash balance held

to finance routine purchases. \(L_T = k\,T\): it is directly

proportional to the value of transactions \(T\) over the period.

RS

Rohan Sharma

M.A. Economics, JNU

Verified Expert

Strategic angle. The transaction demand is best

understood through the velocity-of-money identity \(M_s V = P T\).

Treating \(V\) as roughly constant in the short run pins down the

ratio of money holdings to transactions value, which is exactly

what \(L_T = k T\) says.

Start from the quantity equation: \(M_s V \equiv P T\),

where \(M_s\) is money supply, \(V\) is velocity, \(P\) is the

price level, \(P T\) is nominal transaction value.

Money market equilibrium: \(L_T = M_s\). Combine:

\(L_T \cdot V = P T\), so \(L_T = (1/V) \cdot P T = k \cdot

(P T)\) with \(k = 1/V\).

Therefore transaction demand is exactly proportional to

the value of transactions, with the constant of

proportionality equal to the reciprocal of velocity.

Intuition: a household that ``turns over'' its rupees

more times per year (high \(V\)) holds less average cash

for the same \(T\); a household that pays in cash (low \(V\))

holds more.

Policy hook: if cashless payments rise, \(V\) rises, \(k\)

falls, and the central bank can keep the same nominal \(T\)

with less \(M_s\). This is why digitisation pushes RBI to

re-estimate its money-supply targets.

Why this matters. The transaction demand for money is the

microfoundation of the LM curve, which (with the IS curve) sets the

short-run equilibrium interest rate in the next chapter.

\(L_T = k T\): transaction demand for money is

proportional to the value of transactions, with constant \(k = 1/V\)

where \(V\) is the velocity of money.

Q 2.4

What are the alternative definitions of money supply in

India?

Concept used. RBI publishes four progressively broader

measures of money supply, denoted \(M_1, M_2, M_3\) and \(M_4\).

Each successive measure adds a less-liquid item to the previous

one.

\(M_1 = \) Currency with the public \(+\) Demand deposits with

the banking system \(+\) Other deposits with RBI. This is

the most liquid measure, also called narrow

money.

\(M_2 = M_1 + \) Savings deposits with post office savings

banks. Adds a small but liquid component.

\(M_3 = M_1 + \) Time deposits with the banking system.

This is the broad money concept used as the

principal target of monetary policy in India.

\(M_4 = M_3 + \) All deposits with post office savings

organisations (excluding NSCs).

Liquidity ordering: \(M_1 > M_2 > M_3 > M_4\) in liquidity

but \(M_1 < M_2 < M_3 < M_4\) in magnitude.

\(M_1\) (narrow money), \(M_2, M_3\) (broad money) and \(M_4\)

are RBI's four money-supply measures, each adding less-liquid

items to the previous one.

NK

Neha Kapoor

M.A. Economics, Jawaharlal Nehru University

Verified Expert

Strategic angle. The four measures form a

liquidity ladder: as you climb from \(M_1\) to \(M_4\) you

include progressively less-liquid claims, gaining coverage of

total purchasing power at the cost of timeliness. Each rung adds a

new sub-aggregate of claims that can still be redeemed for cash,

just not as instantly.

Step on rung 1: currency with the public is the

most-liquid claim, instantly spendable.

Add demand deposits (cheque-issuable savings and

current accounts): equally spendable via cheque or UPI.

Add other deposits with RBI (deposits of foreign

central banks, IMF, etc.): small but technically money.

That gives \(M_1\).

\(M_2\) adds post-office savings deposits (almost as liquid

as bank deposits but smaller in volume).

\(M_3\) adds time deposits with banks (fixed

deposits with maturity). They are less liquid because of

penalties for early withdrawal, but they represent

stored purchasing power.

\(M_4\) adds remaining post-office deposits (excluding

NSCs). This is the broadest measure RBI publishes.

Why this matters. Tracking \(M_3\) growth gives RBI a

read on aggregate demand pressures; tracking \(M_1\) growth gives

a read on transactions activity. Each measure has a separate

policy use.

\(M_1 \to M_2 \to M_3 \to M_4\): each measure adds a less

liquid claim to the previous one. \(M_1\) is narrow money; \(M_3\) is

broad money, RBI's main policy aggregate.

Q 2.5

What is a `legal tender'? What is `fiat money'?

Concept used.Legal tender is any form of

money that the law of the land mandates a creditor to accept in

discharge of a debt. Fiat money is money that has value

by government decree rather than by commodity backing.

Legal tender. In India, Reserve Bank of India

notes and Government of India coins are legal tender. A

creditor cannot refuse them in settlement of a debt

denominated in rupees.

Two sub-types of legal tender:

Limited legal tender: coins, accepted only

up to a statutory limit (you cannot pay an entire

large bill in one-rupee coins).

Unlimited legal tender: currency notes,

acceptable up to any amount.

Fiat money. Modern paper currency has no

commodity backing (gold, silver). It circulates because

the central bank declares it acceptable and the public

trusts the central bank's promise. The note itself is

worth very little as paper.

Every fiat-money system also makes the currency legal

tender, but not every legal tender is fiat: gold coins

used to be commodity-backed legal tender.

The Indian Rupee today is both fiat and legal tender.

Legal tender = money law forces creditors to accept;

fiat money = money that has value purely by government decree,

not by commodity backing.

KM

Karan Mehta

M.A. Economics, Madras School of Economics

Verified Expert

Strategic angle. Separate the legal claim (``you must

take it'') from the economic claim (``why it has value''). Legal

tender is the first; fiat money is the second. The two concepts

overlap in modern systems but are conceptually distinct, and

exam questions often turn on the distinction.

Legal tender is a property of the medium set by

law: RBI notes and Government coins for India.

Within legal tender, distinguish unlimited (notes) from

limited (coins above a statutory threshold may be

refused).

Fiat money is a property of the value backing:

intrinsic worth is zero, the value rests on confidence

and on the legal-tender status that compels acceptance.

Historical contrast: gold coins under the gold standard

were commodity money (intrinsic value \(\approx\) face

value); they were also legal tender, but they were not

fiat.

Modern contrast: a bitcoin in India is fiat-like in the

sense that it has no commodity backing, but it is not

legal tender in India because the law does not compel

its acceptance.

Why this matters. The combination ``fiat + legal tender''

gives the central bank both the levers needed to run modern

monetary policy: it can print without commodity-backing limits

and it can be sure the issued notes will circulate.

Legal tender = law-mandated acceptance; fiat money =

value by decree, no commodity backing. The Indian Rupee is both.

Q 2.6

What is High Powered Money?

Concept used.High-powered money (\(H\)), also

called monetary base or reserve money, is the

sum of all liabilities of the central bank that are usable as the

foundation for the rest of the money supply.

In India,

\(H = \) Currency held by the public \(+\)

Cash reserves of banks held at RBI \(+\)

Other deposits with RBI.

Currency is the part of \(H\) that has already escaped into

the public's hands; cash reserves are the part still

held by banks (vault cash plus deposits at RBI).

The money supply \(M_s\) is related to \(H\) by the

money multiplier \(m\):

\(M_s = m \times H,\quad m > 1.\)

Because every additional rupee of \(H\) can support

multiple rupees of \(M_s\) via fractional-reserve banking,

\(H\) is called high-powered.

RBI controls \(H\) through open-market operations

(purchase / sale of government securities) and via its

balance-sheet items (foreign-exchange purchases,

lending to government, lending to banks).

High-powered money \(H\) = currency with public \(+\) bank

reserves with RBI \(+\) other deposits with RBI. It is the

foundation on which the money multiplier builds the broader

money supply \(M_s\).

AN

Anjali Nair

M.A. Economics, IGIDR Mumbai

Verified Expert

Strategic angle. Think of \(H\) as the seed from

which the banking system grows the money supply: only the central

bank can plant new seeds; commercial banks merely multiply them

through fractional-reserve lending.

\(H\) is created exclusively by RBI, on the liability side

of its balance sheet. No commercial bank can manufacture

\(H\).

Once issued, \(H\) either ends up as currency held by the

public (it has left the banking system) or as bank

reserves with RBI (it remains available for credit

creation).

Each rupee of bank reserves can support

\(\dfrac{1}{\text{CRR}}\) rupees of deposits in the simple

deposit-multiplier model. With a CRR of 4%, one rupee

of \(H\) allows up to 25 rupees of deposits.

Cash drain (people keeping more currency, less in banks)

reduces \(m\): the formula \(m = (1+c)/(c+r)\) shows that as

\(c\) rises, \(m\) falls.

Policy implication: an open-market purchase by RBI buys

government bonds from banks and pays in \(H\), raising

\(H\) and (assuming \(m\) steady) raising \(M_s\) by \(m \times

\Delta H\).

Why this matters. The identity \(M_s = m H\) is the

backbone of the entire monetary-policy toolkit: every CRR change,

every OMO and every change in RBI's foreign assets works through

this equation.

\(H\) = currency with public + bank reserves with RBI +

other RBI deposits. \(H\) is ``high-powered'' because each rupee

supports \(m > 1\) rupees of money supply through fractional

reserve banking.

Q 2.7

Explain the functions of a commercial bank.

Concept used. A commercial bank is a

profit-seeking financial intermediary that accepts deposits from

the public and uses them to make loans. Functions split into

primary (accept deposits, advance loans) and

secondary (agency and general utility).

Accepting deposits.

Demand (current) deposits: payable on demand,

cheque-issuable, no interest.

Savings deposits: payable on demand, modest

interest, withdrawal restrictions.

Fixed (time) deposits: payable on maturity,

highest interest.

Advancing loans and overdrafts.

Loans against collateral, cash credits, overdrafts on

current accounts, discounting bills of exchange. This is

the credit-creation function of banks.

Agency functions (secondary). On behalf of

customers: collect cheques and bills, pay utility bills,

buy and sell securities, remit funds.

General-utility functions (secondary). Issue

drafts, traveller's cheques, debit and credit cards;

safe deposit lockers; underwriting; foreign exchange

facilities; ATM and internet banking.

Credit creation. By holding only a fraction of

deposits as reserves and lending the rest, banks

``create money'' in the sense that each new loan

generates a new deposit elsewhere in the system. This is

the foundation of the money multiplier.

Primary functions: accepting deposits (demand, savings,

time) and advancing loans. Secondary functions: agency services

and general utility services. Banks also create money through

the fractional-reserve system.

VP

Vikram Patel

M.A. Economics, Gokhale Institute Pune

Verified Expert

Strategic angle. A commercial bank is best understood as

a maturity-transformation machine: short-term liabilities

(deposits) are transformed into longer-term assets (loans), and

the bank earns the spread. Every other function (credit cards,

forex, lockers) is a by-product of running this machine.

Deposit side: collect liquidity from many savers at low

cost. Demand deposits at near-zero interest, savings at

a small interest, fixed deposits at higher interest.

Diversity of maturities lets the bank manage liquidity.

Loan side: deploy collected liquidity into loans of

various maturities, sectors and risks. The interest

earned exceeds the interest paid on deposits; the gap

(net interest margin) funds operating costs and

profit.

Risk management: the bank screens borrowers, holds

capital against losses and keeps a reserve buffer against

large withdrawals.

Agency and general-utility functions are by-products of

the bank's accounts infrastructure: it already has every

customer's account, so cheque clearing, fund transfers

and forex services come at low marginal cost.

Credit creation: each loan disbursed becomes a new

deposit somewhere in the system, expanding \(M_s\). This

is the macro reason banks are regulated so heavily.

Why this matters. Every part of the money-multiplier

story flows from these functions: deposits become reserves,

reserves are partially loaned out, loans become new deposits,

and so on.

Primary: accepting deposits, advancing loans.

Secondary: agency and utility services. Net effect: maturity

transformation and credit creation.

Q 2.8

What is money multiplier? What determines the value of

this multiplier?

Concept used. The money multiplier \(m\) is the

ratio of the broad money supply \(M_s\) to high-powered money \(H\):

\(m = M_s / H\), equivalently \(M_s = m \cdot H\). It tells us how

many rupees of \(M_s\) are supported by each rupee of \(H\).

Define two key ratios:

\(r = \) reserve-to-deposit ratio (banks' reserves

as a fraction of their deposits; set partly by

CRR and partly by banks' own prudence).

\(c = \) currency-to-deposit ratio (households'

preference for cash vs deposits).

The two-stage balance-sheet derivation in NCERT gives

\(m = \dfrac{1 + c}{c + r}.\)

In the simplest closed-system case where everyone banks

everything (\(c = 0\)),

\(m = \dfrac{1}{r}.\)

With \(r = 0.04\) (4% CRR), \(m = 25\).

Determinants:

Higher CRR or SLR \(\Rightarrow\) higher \(r\)

\(\Rightarrow\) lower \(m\).

Higher excess reserves held by banks

\(\Rightarrow\) higher \(r\) \(\Rightarrow\) lower \(m\).

Hence \(m\) is endogenous: it shifts with household

behaviour and bank prudence, even if the CRR is held

fixed.

\(m = M_s / H = (1 + c) / (c + r)\). Determinants: the

required reserve ratio (CRR), banks' excess reserves, the

public's currency-to-deposit ratio.

SR

Shreya Reddy

M.Sc. Economics, University of Warwick

Verified Expert

Strategic angle. The money multiplier is best derived

from the two identities \(M_s = D + C\) and \(H = R + C\), then

dividing the first by the second. The algebra is short and

brings out exactly how \(m\) depends on the two behavioural ratios

\(c\) and \(r\).

Money supply: \(M_s = \) currency with public (\(C\)) \(+\)

demand deposits (\(D\)). \(M_s = D + C\).

High-powered money: \(H = \) currency with public (\(C\))

\(+\) bank reserves with RBI (\(R\)). \(H = R + C\).

Comparative statics:

\(\partial m / \partial r < 0\) (higher reserve ratio

shrinks \(m\)), \(\partial m / \partial c < 0\) (cash drain

shrinks \(m\)).

Policy reading: when RBI cuts CRR, \(r\) falls and \(m\)

rises; an unchanged \(H\) now supports a larger \(M_s\).

Conversely, festival-season cash hoarding raises \(c\) and

lowers \(m\), contracting \(M_s\) unless RBI offsets with

OMO.

Why this matters. The same algebra explains why the

``effective'' multiplier in India varies from quarter to quarter

even when RBI's announced CRR is constant: households' cash habits

and banks' excess reserves both move.

Money multiplier \(m = (1+c)/(c+r)\). Determined by CRR

(and SLR), banks' excess reserves and the public's

currency-to-deposit ratio.

Q 2.9

What are the instruments of monetary policy of RBI?

Concept used.Monetary policy is RBI's control

of money supply, interest rates and credit to achieve macro

objectives (price stability, growth, financial stability). Its

instruments are split into quantitative (work on

\(M_s\) as a whole) and qualitative (work on the

direction of credit).

Quantitative instruments.

Bank rate. Rate at which RBI lends

long-term to commercial banks; raising it makes

refinance costlier, reducing \(M_s\).

Repo rate. Rate at which RBI lends

overnight to banks against government

securities; the policy rate today.

Reverse repo rate. Rate at which RBI

borrows overnight from banks; floor of the

LAF corridor.

Cash Reserve Ratio (CRR). Fraction of net

demand and time liabilities banks must keep with

RBI in cash.

Statutory Liquidity Ratio (SLR). Fraction

of liabilities banks must hold in approved

liquid securities.

Open-Market Operations (OMO). Purchase or

sale of government securities by RBI in the

secondary market.

Qualitative instruments.

Margin requirements on loans (haircuts on

collateral).

Each instrument changes either \(H\) (OMO), the multiplier

\(m\) (CRR, SLR) or the cost of credit (repo, bank rate).

Quantitative: bank rate, repo, reverse repo, CRR, SLR,

OMO. Qualitative: margin requirements, moral suasion, selective

credit controls, direct action.

AI

Aditya Iyer

M.A. Economics, CDS Thiruvananthapuram

Verified Expert

Strategic angle. Map every instrument to the variable it

moves in the identity \(M_s = m H\): OMO moves \(H\) directly,

CRR / SLR move \(m\), and repo / bank / reverse-repo move the cost of

funds. With this map you can predict the direction of any policy

change in one line.

OMO: a purchase of bonds by RBI prints \(H\); a sale drains

\(H\).

CRR change: raises \(r\) in the multiplier formula and

lowers \(m\), contracting \(M_s\) for the same \(H\).

SLR change: raises required holdings of approved

securities; functionally similar to CRR for \(m\).

Repo rate: this is the price RBI charges for short-term

liquidity. Higher repo \(\to\) higher inter-bank rate

\(\to\) higher lending rate \(\to\) lower credit demand.

Reverse repo: floor for the LAF corridor; sets the

opportunity cost of bank reserves and so the floor for

the call-money rate.

Qualitative tools: targeted at specific sectors (e.g.

higher margin on speculative commodities) when blunt

quantitative tools would over-tighten the rest of the

economy.

Why this matters. These instruments are how RBI

implements its inflation-targeting mandate (4% \(\pm\) 2%

headline CPI). Each policy review tweaks the repo rate and may

adjust CRR / SLR or run OMOs.

Quantitative: bank rate, repo, reverse repo, CRR, SLR,

OMO. Qualitative: margin requirements, moral suasion, selective

credit controls, direct action.

Q 2.10

Do you consider a commercial bank `creator of money' in

the economy?

Concept used. A commercial bank ``creates money'' in the

sense that under fractional-reserve banking each new loan

generates a new deposit somewhere in the system, expanding the

broad money supply \(M_s\) for a given high-powered money \(H\).

Start with a primary deposit of \(\rs 100\) in Bank A, CRR

\(= 20\%\) (illustration only). The bank keeps

\(\rs 20\) as reserves and lends \(\rs 80\) to a borrower.

The borrower spends the \(\rs 80\); the recipient deposits

it in Bank B. Bank B keeps \(\rs 16\) as reserves and lends

\(\rs 64\). The process continues indefinitely.

Geometric series: total deposits created

\(= 100 + 80 + 64 + \dots

= 100 \times \dfrac{1}{1 - 0.8}

= 100 \times 5 = \rs 500.\)

That is, the original \(\rs 100\) of primary deposit has

supported \(\rs 500\) of demand deposits.

Equivalently, \(m = 1/r = 1/0.2 = 5\), and \(M_s = m \times

H = 5 \times 100 = 500\). The banking system as a whole

has ``created'' \(\rs 400\) of new money beyond the

original \(\rs 100\).

Important caveat: an individual bank cannot lend more

than its excess reserves. The money creation is a

system-level property: it emerges when many banks

each lend out their excess reserves.

Yes. Commercial banks collectively create money under

fractional-reserve banking. The process is captured by the money

multiplier \(m = 1/r\) (simple case) or \(m = (1+c)/(c+r)\) (full

case).

MJ

Megha Joshi

M.A. Economics, University of Hyderabad

Verified Expert

Strategic angle. Distinguish ``creation of money'' from

``creation of high-powered money''. Banks create only the former;

RBI alone creates the latter. The two-step illustration below

shows how a single primary deposit grows into a chain of

secondary deposits.

Step 1: RBI prints \(\rs 100\) of \(H\). This is the only

money-creation step that adds to \(H\).

Step 2: Bank A receives the \(\rs 100\) as a deposit.

\(M_s\) now stands at \(\rs 100\) (deposit) but \(H\) is also

\(\rs 100\), so \(m = 1\) for now.

Step 3: Bank A lends \(\rs 80\). The borrower's account at

Bank B credits \(\rs 80\), raising total deposits to

\(\rs 180\), while \(H\) remains \(\rs 100\). Now \(m = 1.8\).

Step 4: Bank B lends \(\rs 64\). Deposits \(= \rs 244\),

\(m = 2.44\). Continuing to infinity gives \(m = 5\) and

\(M_s = \rs 500\).

Single-bank constraint vs system constraint: any one

bank can lend only its own excess reserves. But because

loans return as new deposits at other banks, the system

cycles each loan back as a new asset for the next bank.

The constraint is the system-wide reserve ratio \(r\).

Why this matters. This is the mechanism through which

monetary policy (changing \(H\) or \(r\)) propagates from RBI's balance

sheet to actual money supply growth and from there to aggregate

demand and inflation.

Yes, banks create money. With reserve ratio \(r\),

\(\rs 1\) of primary deposit supports \(\rs 1/r\) of total deposits;

banks collectively turn \(H\) into \(m H\) of \(M_s\).

Q 2.11

What role of RBI is known as `lender of last resort'?

Concept used. The lender of last resort (LOLR)

function refers to the central bank's commitment to lend to

solvent but illiquid commercial banks during a financial panic,

to prevent a contagious bank run.

When depositors lose confidence in a bank, they demand

their money back en masse. The bank's loans are illiquid

(cannot be sold quickly without large losses), so a

solvent bank may still fail purely for lack of cash.

As LOLR, RBI provides short-term liquidity to such banks

against good collateral (government securities,

approved bills), usually at a penalty rate

(Marginal Standing Facility, MSF).

Conditions historically associated with LOLR (Bagehot's

rule):

Lend freely.

Against good collateral.

At a penalty rate.

Only to solvent (not insolvent) institutions.

By guaranteeing emergency liquidity, RBI prevents

runs on healthy banks from spreading; the mere knowledge

that LOLR exists keeps depositors calm.

Modern variants of LOLR include the MSF window, the

Liquidity Adjustment Facility (LAF) and special

liquidity windows during crises (e.g. COVID-19

targeted long-term repo operations).

Lender of last resort: RBI lends short-term to solvent

but illiquid banks during panics, against collateral and usually

at a penalty rate, to prevent contagious bank runs.

RB

Ravi Bhardwaj

M.A. Economics, Ambedkar University Delhi

Verified Expert

Strategic angle. LOLR is the central bank's role as the

ultimate provider of liquidity: the safety net that

prevents a liquidity squeeze from turning into a solvency crisis

and a single failing bank from triggering a system-wide panic.

Run a thought experiment. Imagine 20% of a bank's

depositors withdraw on the same day. The bank's loans

cannot be sold instantly without large losses; without

external liquidity it would have to suspend payments.

Without LOLR, news of one bank's suspension spreads,

depositors at other banks rush to withdraw, and the

liquidity shock becomes a system-wide bank run.

Enter LOLR: RBI accepts the suspended bank's good

collateral (government securities, AAA bills) and

advances cash. The bank meets the rush and re-opens.

Penalty rate matters: by charging more than the market

rate, RBI ensures that banks treat LOLR as a last

resort and not as a routine funding source.

Limits: LOLR cannot save an insolvent bank

(one whose loan losses exceed its equity); for those,

deposit insurance and resolution authorities take over.

Why this matters. LOLR is one of the three classical

roles of a central bank (currency issue, monetary policy, LOLR).

A board-exam answer that lists all three earns full marks even on

short questions.

LOLR role: RBI provides emergency liquidity to solvent

banks against good collateral, usually at a penalty rate, to

prevent panic-driven bank runs.

NCERT Solutions Class 12 Economics Chapter 3 Money and Banking FAQs

Ques. How many questions are there in NCERT Class 12 Economics Chapter 3 Money and Banking?

Ans. There are 11 end-of-chapter exercise questions in NCERT Class 12 Economics Chapter 3 Money and Banking. All 11 questions are solved with full step-by-step working in our money and banking class 12 ncert solutions PDF. The mix is roughly 8 theory questions and 3 numericals, with the heaviest marks on Q9 (instruments of monetary policy of RBI) and Q10 (credit creation by commercial banks class 12).

Ques. What are the four functions of money in Class 12 Macroeconomics?

Ans. The four functions of money in money and banking class 12 are medium of exchange, unit of account, store of value and standard of deferred payment. The first two are primary functions and solve the double-coincidence-of-wants problem of barter; the last two are secondary functions that allow purchasing power to be carried across time and used as the basis of credit contracts. This four-function split is the most-asked one-mark question from money and banking class 12 in CBSE board papers.

Ques. What is the money multiplier formula in Class 12 Economics?

Ans. The money multiplier formula is m = 1 / r in the simplified no-cash-drain case, where r is the cash reserve ratio (CRR). With a currency-to-deposit ratio c included, the full formula is m = (1 + c) / (c + r). Money supply is then Ms = m times H, where H is high-powered money. CBSE Class 12 Economics numericals almost always use the simplified m = 1/CRR form, and our money and banking class 12 questions and answers PDF works every example with the formula written on a separate line for the method mark.

Ques. How do commercial banks create credit in Class 12?

Ans. Credit creation by commercial banks class 12 works through the deposit-loan-redeposit chain. A primary deposit of Rs 1,000 with CRR of 20% lets the bank keep Rs 200 as reserves and lend out Rs 800. The Rs 800 is spent and redeposited into the banking system, where 20% (Rs 160) is held as reserves and Rs 640 is lent again. The chain continues until total deposits reach Primary Deposit / CRR = Rs 5,000. The bank has therefore created Rs 4,000 of derivative deposits, which is why commercial banks are called creators of money in the NCERT textbook.

Ques. What are M1, M2, M3 and M4 in supply of money class 12?

Ans. M1, M2, M3 and M4 are the four progressively broader measures of money supply published by the RBI. M1 equals currency with public plus demand deposits plus other deposits with RBI (the narrowest, most liquid measure). M2 adds post office savings deposits. M3 equals M1 plus net time deposits with commercial banks and is called broad money, the measure the RBI targets in monetary policy. M4 adds total post office deposits and is the broadest measure. The ordering M1 < M2 < M3 < M4 is a frequent CBSE one-mark question.

Ques. What are the instruments of monetary policy of RBI in Class 12?

Ans. The instruments of monetary policy class 12 fall into two families. Quantitative tools (six) are bank rate, repo rate, reverse repo rate, Cash Reserve Ratio (CRR), Statutory Liquidity Ratio (SLR) and Open Market Operations (OMOs). They act on the total volume of credit. Qualitative tools (four) are margin requirements, moral suasion, credit rationing and direct action; they act on the direction of credit toward specific sectors. CBSE Class 12 Economics asks this list as a 6-mark question almost every alternate year.

Ques. What is high-powered money in Class 12 Economics?

Ans. High-powered money (H), also called reserve money or monetary base, is the foundation of the money supply. It has three components: currency held by the public, cash reserves of commercial banks held with the RBI, and other deposits with the RBI. The textbook formula is H = Currency with Public + Bank Reserves with RBI + Other Deposits with RBI. Money supply equals m times H, where m is the money multiplier. Skipping the "other deposits with RBI" term in Q6 of the NCERT exercise is the most common mistake students make on this question.

Ques. What is the difference between repo rate and reverse repo rate?

Ans. Repo rate is the rate at which RBI lends short-term funds to commercial banks against government securities; a higher repo rate makes borrowing costlier and contracts money supply. Reverse repo rate is the rate at which RBI borrows from commercial banks; a higher reverse repo absorbs liquidity from the banking system. Both are quantitative instruments of monetary policy of RBI, and their gap (the repo corridor) defines the operating stance of monetary policy. CBSE Class 12 Economics has tested this distinction in three of the last five board papers.

Ques. What is legal tender and fiat money in Class 12 Macroeconomics?

Ans. Legal tender is money that, by law, must be accepted in payment of debts; in India, currency notes issued by the RBI and coins issued by the Government of India are legal tender. Fiat money is money declared by government decree to be money, with no intrinsic value (it is not backed by gold or silver). The Indian Rupee is both legal tender and fiat money. CBSE Class 12 Economics tests this distinction as a 3-mark theory question in alternate years, and Q5 of the NCERT Chapter 3 exercise asks for one-line definitions of both.

Ques. What is transaction demand for money in money and banking class 12?

Ans. Transaction demand for money is the cash people hold to meet their day-to-day buying needs between two consecutive income receipts. It is captured by the linear relation LT = k times T, where T is the volume of transactions and k is the fraction held in cash form. Transaction demand rises with national income because higher income supports higher transactions. The NCERT chapter Q3 tests this relation, and CBSE markers expect students to derive LT = kT on a separate line before linking it to national income for full marks.

Ques. Why is RBI called the lender of last resort?

Ans. RBI is called the lender of last resort because, under Bagehot's rule, it lends to solvent but illiquid commercial banks during a financial crisis when no other lender is willing. By doing so, RBI prevents a temporary liquidity shortage from becoming a system-wide bank run. This is one of the four central bank functions covered in Chapter 3 of NCERT Class 12 Economics, and Q11 of the exercise asks students to define this role in 3 to 4 sentences with the Bagehot reference for full marks.

Ques. Is the Class 12 Economics syllabus changing for 2026-27?

Ans. No major reductions in 2026-27. The chapter structure of the Introductory Macroeconomics textbook is unchanged for the current cycle, and the CBSE marking scheme continues to reward step-by-step formula working in numerical questions. Our money and banking class 12 ncert solutions for the 2026-27 cycle are aligned to the unchanged textbook and the latest CBSE sample paper released for the 2026 boards. The four functions of money, the M1-M4 measures, the money multiplier and the instruments of monetary policy of RBI are all preserved as-is for 2026-27.

Comments